Singapore market went through a mini rollercoaster ride in the past 3 months, going up to 3300 then down to 3100 and now back to 3200 again. Trade war seems to have no impact on the US markets as they kept breaking all time high.

From this quarter onwards, we will be discontinuing Quarterly Results Review - it seems to have became a "for the sake of writing" commentary providing only basic information without much substance. Instead, we shall integrate important portfolio developments in the Quarterly Performance Review.

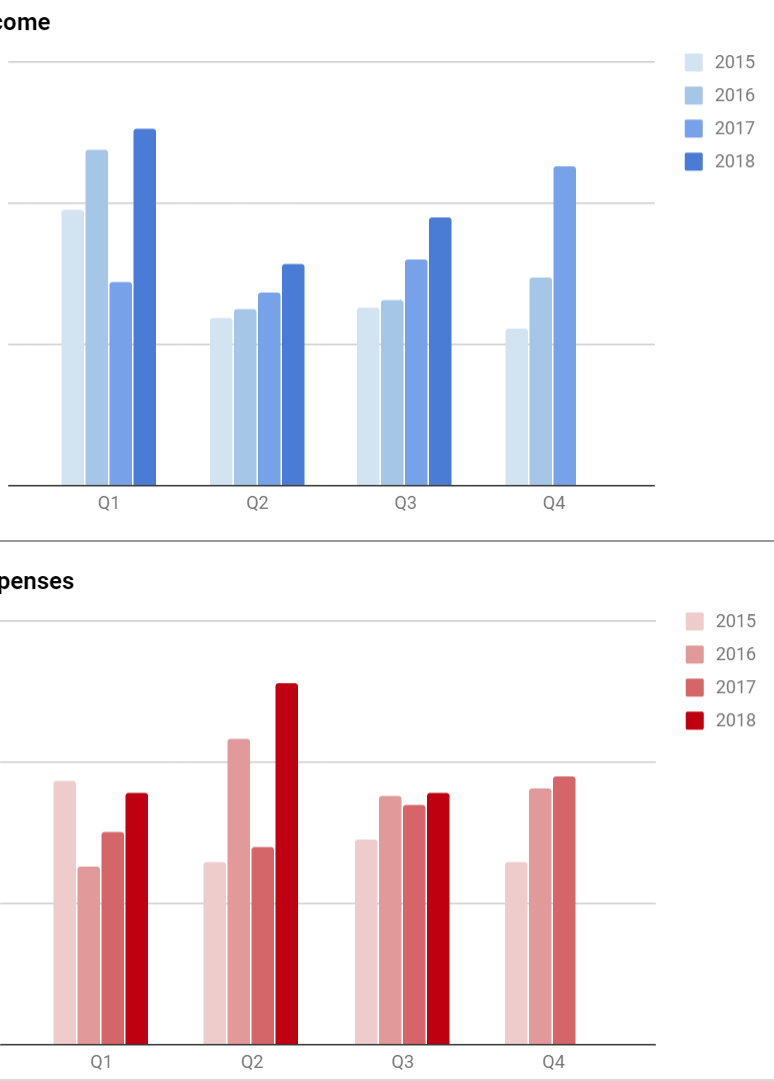

Performance Review Highlights

Our portfolio was saved by the buyout offer of M1 shares (on the last day of Q3!), raising its value nearly 30% in a single day. Entire portfolio value skyrocketed $3700, which I believe is the largest ever single day increase.

We are down 4% year to date compare to 1% down of the STI, mostly dragged down by Kimly. Excluding this stock, we would be nearly even. Would our growth assessment of this coffee shop business come true? Or will this huge position left a huge scar in our portfolio? Only time will tell and 2019 should be a game changing year.

We gave out $2600 worth of dividends (thanks to a massive distribution from Singtel) which is once again our best Q3 yet. This will be a record-breaking year of dividends!

Another all-time high quarter - Higher salary, higher passive income and even higher one-time income due to a recontract of mobile plan and selling iPhone for $560 profits. Unfortunately, the expiry of our old corporate plan also meant a much higher monthly recurring cost.

This was a big mistake on hindsight. I did not do enough research before re-contracting, and in the aftermath realized there were much cheaper SIM only plans with huge data, and cost only like $30 in the market. Instead, what I got was a $60 plan with upfront $560 "profits" to spread out the cost.

All in all, it wasn't worth it. I was tricked into believing:

1. My corporate plan discount was higher than what was advertised (turned out the promotion expired like 3 days before I recontract) I did not re-confirmed the discount rate again when I signed.

2. False advertising by a very enthusiastic Citibank Credit Card salesguy, mislead me into believing the benefits are good when there are many terms and clauses making it difficult to hit the advertised rebate rate (common trick by many banks. Haiz. I should have been more aware.)

This mistake is probably going to cost me hundred dollars or so, and lesser data/month for the next 2 years. I really learnt my lesson from this. Always double check!

Operating Highlights - Expenses

Recurring expenses/one-time expenses were both in-line with the past 3 years, with the traditional August angbao for Mum.

Acquisitions & Developments

We brought Kimly early this quarter based on the same proposition:

Kimly - Defensive consumer staple with strong cash flow, high cash balance and organic growth prospects. This is more of a capital-gain and opportune play.

Operating Updates

Finally decided to do a little streamlining by closing our OCBC360 account. The $3000 could be better off earning $5/mth in DBS Multiplier compared to $0.70 per month in OCBC360.

We delayed so long mainly due to GIRO and other stock crediting arrangements, but now I realize it's not that difficult to switch. Everything can be done online and essentially a new submission will overwrite the previous. This will also reduce the hassle of transferring small amounts here and there just to pay different bills every month.

With that, we officialy say goodbye to OCBC360 which has accompanied us for more than 5 yrs.

Outlook

2018 is shaping up to be another milestone year as we break major goals: "25 years expense" holy grail, 5 digits passive income and more. Looking forward to the annual report!

Some stocks on our watchlist include:

STI ES3 (3.2), ST Engineering (3.2), Capitaland (2.8), Sembcorp Ind (2.5 or 75% of book value), Mapletree Commercial Trust (1.55), Singtel (3), Raffles Medical Group (0.9), Far East HTrust (0.6 or 6.5% yield), Frasers Property (Below 1.6, NAV at 2.45, 8.6c dividend over 5% yield)

No comments:

Post a Comment