Presenting 2016 Annual Financial Report!

Note From CEO

It has been a year of ups and downs. We moved to a new revenue source (hopefully with better prospects), realized significant capital gains and held on through the unpredictability of the market.

Important highlights:

- We achieved record earnings, and our net asset value grew by over 33%.

- Our overall saving rate of the year stood at 78.2%.

- Our safety passive income now covers 28% of our expenses.

- Our XIRR for 2016 is 15.6%, the first positive year since inception.

- We generated over $3000 (approximately $250 per month) worth of dividends in 2016.

For more details, please refer to specific section of the report.

*All figures exclude CPF and investment capital gains/losses.

-------------------------------------------------------------------------------------------------------------------------

Comparison With Previous Year

Expenses overall was 16% higher compared to previous year, with the most significant expenses being:

- One Time Loss, Samsung Galaxy S7, Mayday Concert in Q2

- Parent Gift in Q3.

- Braun Shaver (9 Series) and Medical Consultation in Q4

Income was 14.1% higher than the previous year, arising from:

- Record bonus in Q1.

- Structural revamp (leave encashment and pro-rated bonus) in Q4.

- Overall higher income throughout the year.

-------------------------------------------------------------------------------------------------------------------------

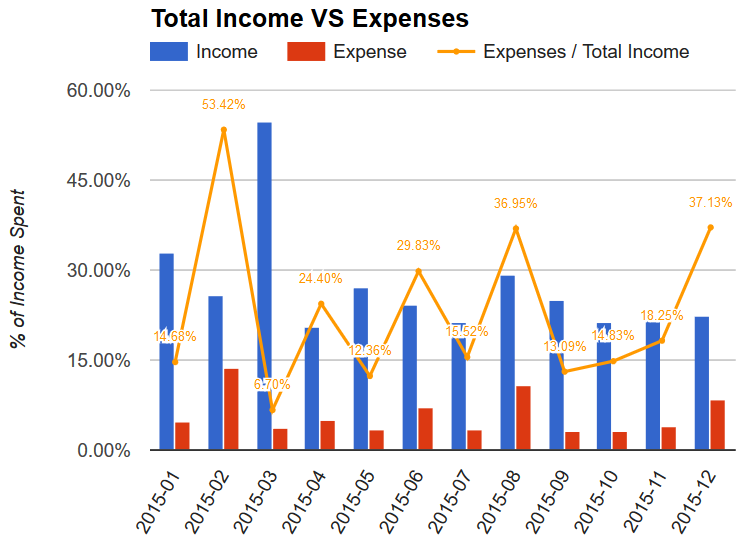

Total Income VS Total Expenses

Expense were stable except for the month of May (one-time loss).

For the whole year, our expense as percentage of income stood at 21.8% (Comparable with 21.4% in 2015). In other words, we have a saving rate of about 78%.

We achieved a record operating income and hence profit for the year (highest ever), and we do not expect to duplicate this performance anytime soon (at least not for 2017).

-------------------------------------------------------------------------------------------------------------------------

Passive Income VS Recurring Expenses

This section strips out the "noise" and highlight only the recurring portion of expenses against passive income.

It removes 3 main categories of expenses as compared to above:

1. Special - Major Items (mostly any non-essentials above $200, but not all), Gifts

2. Vacation - Any overseas trip

3. Tax - You do not get tax on capital gains/dividends in Singapore

It includes only the following form of income:

1. Dividends (Listed and Unlisted)

2. Regular Bank Interests (except special 1-time promotions)

And excludes all the following form of income:

1. Salary

2. Gambling

3. Angbao

4. Rebates - Any form of credit card or purchase rebates

5. Sale of any items

6. Rewards - Such as IPPT, RT payments, etc...

To be honest, I'm freaking amazed by the results. I'm doing much better than I imagined, and I would never have known if it weren't for all the effort put into tracking them.

There were 2 months (May and August, traditionally the 2 strongest dividend months) where my passive income exceeded my recurring expenses.

For Year 2016, my passive income is now sufficient to cover just over 56% of my recurring expenses (compared to 50% in 2015). Adding in the "double safety margin" criteria, it can cover 28% of my expenses.

-------------------------------------------------------------------------------------------------------------------------

Recurring Expenses Breakdown

As always, my top expenses are food, personal (clothing, self consumables), travel (transport) and utilities (internet and phone).

Some random discoveries:

1. I visited an "alcoholic outlet" and purchased a beverage only twice this year.

2. I brought 31 cups of Bubble Tea (i.e Koi, Gong Cha) 31 times this entire year, which costs me $106.50 in total.

3. I brought 23 cups of Cafe drinks (i.e Starbucks, Coffee Bean) this year, and each cup averages $4.80 (I usually only drink when there's 1 for 1 deal).

4. I ate fast food (counting lunch, dinner, supper) 81 times this year (!!!). To be frank, this figure is a bit higher than I thought and is not very healthy. Hopefully I can cut it down to perhaps 60 times or less.

5. I visited a restaurant 32 times this year (That's about 2 or 3 times a month, lower than most youngsters these day I believe). Each restaurant trip averaged $20.10.

6. I visited the KTV only 8 times (less than once a month) this year, each trip averaging $21. I should go to Neway more often.

-------------------------------------------------------------------------------------------------------------------------

Our portfolio is up 18% while STI is up roughly 3.5%. Since IPO, our portfolio is at a breakeven status while STI is down about 8%.

A majority of our returns this year came from the privatization of China Merchant Pacific (CMP)/Super Group and sale of ST Engineering. On the other hand, we suffered the most losses from the "collapse" of M1 (with confirmation of 4th Telco).

In terms of acquisitions, we added Frasers Centrepoint Ltd in Q3 and Singapore Telecommunications in Q4 - both which are long-term dividend holdings we are very confident of.

For the entire year, the portfolio generated just over $3000 of dividends, $600 higher than last year (lower than expected). This was largely due to the events above: In exchange for capital gains, we lost the 2 dividend cash cows of CMP and ST Engineering (both listed and unlisted holdings).

As of now, we still hold the majority of our assets in Cash. Our equities portfolio remains healthy and diversified, with top holdings being FCL, FCT, Singtel and STI.

-------------------------------------------------------------------------------------------------------------------------

Outlook For 2017

We will continue our strategy to build a sustainable and diversified dividend portfolio in 2017. With news of 3 rate hikes incoming, there will be plenty of opportunities to pick up bargains in the market.

As the company is holding a large proportion of cash, we intend to deploy them as soon as reasonable (projected 3 bullets in the first half of the year) to meet the dividend targets for next year.

Financial Goals For 2017

- Attain $5000 worth of dividends (depending on state of market)

- Increase STI as a core holding to 25% of our portfolio for stability and defensiveness.

- Explore other forms of investments (Robo) and perhaps Singapore Saving Bonds.

{kind=link}