There are many articles regarding the arduous and greatly misunderstood path of financial freedom. Often, it is not only about the struggles of saving and financial prudence, but a lot more comes from society pressure, norms and expectations.

I can really feel the reader's struggles from his letter - it's something that is just not widely accepted in a society like Singapore.

It's similar to "expectations" to get married (despite it being a VERY BAD DECISION if you do it for the sake of doing so), expectations to "get a job", expectations to "climb the ladder". If you have no ambitions to chase these things, you're considered a "good for nothing" or "lazy bum".

I shall walk my own path - 不在乎世俗的眼光

“Creating a life that reflects your values and satisfies your soul is a rare achievement. In a culture that relentlessly promotes avarice and excess as the good life, a person happy doing his own work is usually considered an eccentric, if not a subversive. Ambition is only understood if it’s to rise to the top of some imaginary ladder of success. Someone who takes an undemanding job because it affords him the time to pursue other interests and activities is considered a flake. A person who abandons a career in order to stay home and raise children is considered not to be living up to his potential — as if a job title and salary are the sole measure of human worth.

You’ll be told in a hundred ways, some subtle and some not, to keep climbing, and never be satisfied with where you are, who you are, and what you’re doing. There are a million ways to sell yourself out, and I guarantee you’ll hear about them.

To invent your own life’s meaning is not easy, but it’s still allowed, and I think you’ll be happier for the trouble.”

On the positive side of thing, an interesting comment from the article by BigCatBlue:

"As an investor, I need people to believe in working and spending. Do it as much as possible. In put it crudely, greed is good.

Imagine if the companies that I have invested in found out that most people, if not all people are financially secured. They don't need to slave over a mortgage, put good food on the table, upgrade their car and condo, and enjoy all the trappings life can offer. Employees will revolt! Who then will work for me while I collect dividend and enjoy a slower pace in life?

Masses of people thinking of financial independence -- that I am afraid. Please labour on for our sake."

M1

Results continue to dip, but IMO it is actually not bad. There are signs of it bottoming (for now), with net profit declining 5% year on year. For 9 months it is down 13.5% (9M EPS from 12.6c to 10.9c), which seems to be in line with the stock price ($2 to $1.8). Service revenue increase 5% and mobile ARPU remain stable at $55. Mobile customers base fall due to shutdown of 2G network, and overall their market share is still stable at 25%.

They launched lots of initiatives this past quarter like malware detection solutions, nationwide IOT, smart sensors etc which would all take time to materialize. Yield at $1.8 is 6.1%, based on trailing results. The million dollar question is if they can sustain the current DPU.

Afternote: More news of first "intelligent" waste management system, cloud offering of digital startups. I might consider averaging down if I sell other position.

CapitaCommercial Trust

DPU still went up 2.6% despite selling away 3 buildings. This is the definition of a well managed REIT. Subscribed for their rights. Main catalyst now is Golden Shoe redevelopment and how they can bring Asia Square Tower 2 forward.

Afternote: For some unknown reason, CCT had a crazy run-up after the rights issue to over $1.8. The pro-forma NAV is $1.76 and 1H2017 DPU is 4.23 cents (annualized 8.46 cents). Considering a 9c DPU yearly, the yield is barely ~5%. This makes me really tempted to just sell it.

I believe it would be more fairly valued at $1.65 for a 5.5% yield.

CapitaMall Trust

A very flat quarter with regards to DPU, shopper traffic and tenants sales. Expect stable 11c DPU (5.4% yield at $2.04) until the launch of Funan in 2019.

Frasers Centrepoint Trust

Full-year DPU rose 1.2 per cent to 11.90 cents, the highest since the FCT's listing in 2006. Integration with Northpoint City North Wing is in its final stages.

My crown holding - low debt level (29%), 11 years of increasing DPU, NAV grown from 1.78 to 2.02 since I first vested in 2014, best management, super resilient. Every single quarter the results is good. What more can you ask for?

Stock price has reached an all time high (>$2.20) that sometimes, I am tempted to sell it in hope of getting it back at a lower price.

Far East Hospitality Trust

DPU falls 8% to 1.03c but the stock keeps going up - probably in anticipation of recovery next year (revenue for hotel rooms went up). There is also the acquisition of Oasis Downdown mid next year which is expected to be slightly accretive.

Sembcorp Industries

Saw a 37.7% drop in net profit due to several one off items - non-cash impairment charges and 11m of doubtful debts write offs. Marine show small profits again after losses last year.

Overall I think the company is stabilizing (Operation Profit up 11% for 9 months) and management indicate strategic review will be completed soon. NAV is up from $3.58 to $3.86.

Singtel

Only 3c special dividends (from about 14c gain) from Netlink IPO, on top of standard 0.68c (60% payout) dividends. Excluding Netlink, earnings fell 4% mainly due to intense competition in India.

Still feel confident that it should trade between $3.6 to $4.

Afternote: Fair results, down trending price? Singtel is the number 1 stock in Singapore by market cap, and deserve to at least trade at a "fair value". I strongly believe $3.6 can hold and increased my position again seeing the continued drop. Look forward to my 9.8c dividends in January next year.

Frasers Centrepoint Limited

Dividends maintained at 8.6c per year (60% payout ratio) and delivered yet another solid quarter with revenue/profit increasing 17%. NAV is now at $2.46.

Like that they are diversifying their income to now over 50% outside Singapore, and concentrating on growing their recurring income. This is the best "ETF" I ever brought.

Accordia Golf Trust

Ah! The big surprise this quarter. DPU plunged over 30% due to "unusually large return of members' deposit" despite profits and revenue going up. Hopefully this is a one time event.

To add further uncertainty, golf utilization fell ~15% as they were closed for 10 days due to typhoon in October. It does not sound good for their next quarter in view of the harsh winter ahead.

Given that I am comfortably in the money, I will hold and see.

Netlink Trust

Nothing much to say - everything according to forecast results and on track to meet target DPU.

Watchlist

Comfort Delgro - $1.9 and below would be extremely tempting.

SGX - Closer to $7.

Raffles Medical Group - Closer to $1.

Starhill Global Reit - 6.5% yield at $0.75.

Mapletree Comm Trust - Below $1.5, camping at 6% yield. NAV is $1.37.

ST Engineering - Would likely bite at 5% yield (closer to $3)

Capitaland - Look closer to $3.3 or below.

Mapletree Greater China Trust - $1.1 or when it retract to more than 7% yield.

Over the past year, I'm getting bombarded by more and more newsletters, articles, emails and services. There are so many overlapping stuff and it's a real pain in the neck dealing with all the good and bad sources.

Hence, I'm taking this chance to consolidate these sources and pick out the cream of the crop.

Portfolio Tracking

To track our portfolio performance, monitor price changes. The ease of use, accessibility ,and user interface is of almost importance.

1. Yahoo Finance - A much inferior choice, after they brought down Google Finance.

2. SGXCafe - Favourite for monitoring day to day changes (email) and comprehensive reports.

Eliminated: Google Finance (was the best, until they decide to terminate it), MoneyMSN, Stockflock

Generic Stock News

We all need constant source of ideas to feed our minds.

1. Feedly - My personal consolidated source of around 100 blogs. I go here for inspiration and ideas.

2. Motley Fool - Promote long term investing but articles tends to get repetitive.

Analyst Reports & Price Targets

Professional analyst reports. Take them with a pinch of salt, but good reference for information.

Stock Information

1. Dividends.sg - Best consolidated dividend hsitory

Forums & Social

1. SSI and MoneyMind

2. InvestingNote

Mobile Apps

1. Spiking - Tracks 'big names' buys and sells

2. SGXMobile - Notification of company announcements

3. SG Stock Alert - Notification of company announcements

Procedures Before Buying

1. Search Info at Dividends.sg (dividends history, recent announcements)

2. Analyze company (latest results)

3. Read analyst reports and any other news

Performance Highlights

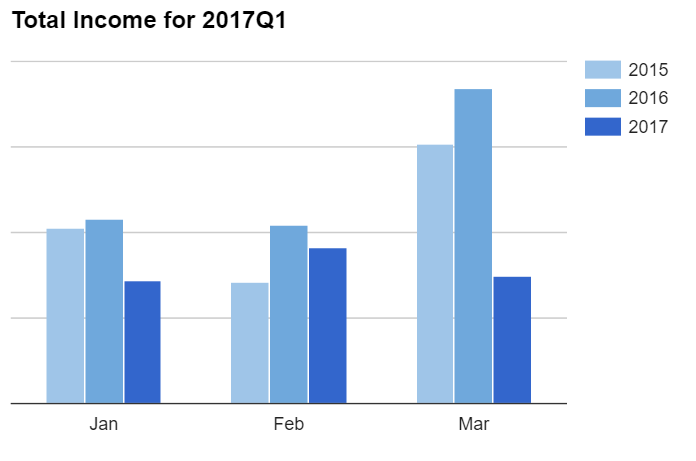

STI inches up slightly in Q3 by 0.8% while the Dow Jones continue to break historical high despite tensions with North Korea. Our portfolio grew by 0.5% with most coming from dividends. No major acquisitions in Q3 except for a very small stake in Netlink Trust gotten from IPO. Our assessment is still that the SG Market is fairly valued now, although some blue chips are falling into bargain territory.

We paid out dividends of over $1500, the highest ever for a single quarter. This is almost doubled the same period last year.

Operating Highlights

The most important milestone is that we have officially secured our revenue source, extending our lease expiry by another year. It comes with a good positive renewal, affirming the board's strategic decision last year.

Income for the quarter was about 23% higher largely due to mid year bonus in July. Other one-time revenue came from the numerous IPT sessions in August. We expect income to be higher in Q4 as well from the year end bonus, which should make up for the loss in Q1 this year.

Overall, total income this year should be comparable to last year.

Expenses were about 5% lower, with the only major expense being our traditional parents gift in August. August expenses would almost always be the highest in the year. If we exclude that, our fixed expenses would probably be some of the lowest 3 month period.

We do not foresee any major expense coming up for the rest of year, except the slight possibility of getting a laptop for work purposes.

Acquisitions & Divestments

We came very close for a few purchases but it always seem to slip us by, and now our cash holdings are almost back to Q1 level. The only purchase this quarter is a very small stake in Netlink Trust.

CapitaComm Trust would be doing a rights issue soon and while we are slightly doubtful of the acquisition (non DPU accretive), analysts claim it will be beneficial in the long term. That said, we see no reason not to sign up for it. Closing date is 19th October.

The general intention would be to once again deploy more into investments in the next 3 months, especially since we anticipate more cash inflow.

This is a first world problem. We are still deciding if we should make do with a little less margin of safety and make more "fair value" purchases instead of waiting for huge bargains.

Outlook

We have a long list of potential acquisition targets and prices that would warrant us to "take a closer look".

Comfort Delgro - This transport giant has fallen >30% from its $3 peak. Management guided declining revenue in almost all segments, and it is plagued by competition from Grab. However, we must know that only 30% of revenue comes from Taxis. Buses and MRTs are still largely profitable, and there must come a point where valuation is cheap enough to worth it. $1.9 and below would be extremely tempting.

SGX - Closer to $7. Monopoly business with a stable and safe 28c DPU per year. The problem is how much yield is sufficient to reduce capital-loss risk? We think 4% is fair while not being over excessive.

Raffles Medical Group - Closer to $1. Despite crashing near 40%, it is not really that cheap based on historical valuation (its PE is around 23, right around the 5 year mean). More investors are cutting back expectations after management guided "3 years turnaround time" for China operations. We are lacking healthcare exposure and still largely believe in RMG growth story in the long term (5 to 10 years). However, we need a good margin of safety, especially when this is not a dividend stock (1+% yield).

Starhill Global Reit - DPU was about 10% lower last quarter due to large number of AEIs. DPU per year should range around 4.92c to 5c range, which gives around 6.5% yield at $0.75.

Mapletree Comm Trust - Below $1.5, camping at 6% yield. Vivo City is a shopping paradise (well-managed and diversified, especially with the upcoming AEI) and Mapletree Business Centre is just icing on the cake. NAV is $1.37, so the key is just to not pay too high a premium.

ST Engineering - Compared to Singtel which has a higher yield of 4.7% (at $3.68) and lower payout ratio, ST Engineering just doesn't seem as appealing at $3.4. Their dividends are safe but stagnant. I have been looking to join back this solid Ah Gong company for a long time. and would likely bite at 5% yield (closer to $3)

This was a song that I overlooked when Mayday new album came out. Pretty much skipped it, largely because the melody wasn't too appealing the first few times I heard it.

That was until it won the Best Lyrics Award (caught my attention), and then subsequently the 2nd version of the MV came out.

Now, it has grown on me so much that it's becoming one of my favourite songs on the new album.

Viewed narrowly, the lyrics are obviously talking about the hardship Mayday have gone through to pursue their music dreams.

Viewed from a wider perspective, it can be a reflection of many goals we pursue in life. Our commoner life may be nowhere as exciting or dramatic as theirs, but some of the lines in this song really shook and touched me on a personal level.

Every battle relies on guns and food. Can passion alone feed your stomach? Can love exist without bread?

Pursuing your dreams wholeheartedly is like watering the dry and barren soil of reality with blood, sweat and tears. It may not yield any results.

Can you persevere in the face of harsh reality?

And should the day come when you arrive at your goal, would you be as happy as you thought? Or are you just stepping into another jail? Another rat race?

一双又一双的目光 像监狱和高墙

墙里的风光是不是 如当初想像

You will be judge by others. By society norms. By peer pressure. And ironically, the older we get, the more we are afraid of being judged.

Can we find back our younger self? The one who is "stupid" but strong?

Are we really wiser as we grow older? Or have we lost something in the process of growing up?

I have no intention of using the advanced strategies covered, but post here solely for my reference.

---

Now that the basic is covered, let's talk about strategies. There are strategies for existing shareholders who already holding shares before the rights exercise is announced, and there are also strategies for people who want to take advantage of the rights to get into the company at a favourable time. These are the wannabe shareholders. I must say rights issue favour the latter rather than the former. That's just the way it is.

I further define two types of player: the casual and the advanced one. Casual ones are usually newbies, but need not be, and quickly wants to get over the rights issue as soon as they can. Advanced players want to hack the rights and get a more favourable price, meaning getting their average price below the theoretical ex rights price (TERP).

w: no of mothers shares before XR

x: no of rights shares successfully subscribed

y: price of mother shares before XR

z: subscription price of rights shares

TERP = [(w*y)+(x*z)] / (w + x)

As you can see, to get a lower average price, you need to get much more excess rights beyond the rights ratio. If the rights ratio is 166 shares for every 1000 shares held before XR, to get a lower price than TERP, you need to get more rights shares than 166.

Link for casual rights player: here

Link for advanced rights player: here

For existing casual shareholders:

a. Just wait for offer information statement (OIS) to come in. It'll inform you of the number of entitled rights shares you have.

b. Go atm and subscribe to the entitled rights

c. At the same time, apply for the excess rights. There's also a $2 admin fee charged by every bank.

For existing advanced shareholders:

1. Sell all your mother shares before XR, buy back after XR and after the price drops lower than TERP

2. Buy more mother shares before XR and take adv of the drop in price, be entitled to more rights, apply for excess

3. Buy nil paid rights during nil paid rights trading period, esp when there are opportunities for arbitrage, subscribe to entitled and also apply for excess

* 2 and 3 can be combined, but make sure you know what you're doing

For casual wannabe shareholders:

a. Buy the mother shares before XR

b. Wait for OIS to inform you how much entitled rights you have. If you bought too close but still before XR, the OIS might not reach you on time. So calculate manually.

c. Go atm and subscribe to the entitled rights

d. At the same time, apply for the excess rights

For advanced wannabe shareholders:

1. Buy in after XR, at or below TERP, and skip all the rights exercise

2. Buy in before XR, get your entitled rights, apply for excess by maximizing rounding

Since preference is given for excess rights applicants to round off odd lots, and assuming that the rounding of odd lots is for 100 shares per board lot, it make sense to change the number of shares you want to buy before XR to maximise the odd lots rounding. For example, if you get 1000 shares before XR, you are entitled to get 166 excess. To round off to the next nearest round lots, you are almost guaranteed to get 34 excess rights (to round to 200 shares). Can we maximise that rounding so that you can get the best out of it?

In the past, where the board lot is 1000 shares, there's some savings to be had, but not anymore.

Just ignore this method safely, knowing that you are not going to hack a lot to get a lower average price using this method.

3. Buy nil paid rights during nil paid rights trading period, subscribe to entitled

* 2 and 3 can be combined, but make sure you know what you're doing

I am experiencing my first Rights Issue with Capital Commercial Trust soon, and have scouted around the financial blogsophere for information on how to do this properly.

This post is not meant to address the specifics of CCT rights issue, but more a general guide on how rights work and how to apply for it.

Credits mainly to BullyTheBear, with bits and pieces of information from other sources.

----

1. Rights Issue Announcement

With rights issue announcement, the most important is the "X rights per Y shares at Z price" information. Upon the subscription of rights, the nil paid rights (named because you have not subscribed to it; you are just holding the rights) will convert to ordinary shares / paid rights.

4 Choices when right issue happen:

1. Sell your shares before the "ex-rights" date. (Before this date, all shares will include the value of the rights)

2. Subscribe. Otherwise, you risk facing dilution.

3. Sell Your Nil-Paid Rights (or buy more) during rights trading period. (Usually complicated and not worth the effort. Pay commission + short trading period)

4. Do nothing. (Worst option. Wasting money.)

If you want to subscribe, you have until the "Close of Rights Issue" date to press at the ATM.

---

2. Rights Trading

With "renounceable" rights, you can sell them off. For "non-renounceable" (also known as preferential offering), you can't. What price to pay for the rights?

This is for if you really want to do trading for the rights,

Nil paid rights price + Subscription price = Price of mother shares after XR

"The subscription price for this cct rights exercise is 1.363. Let's say upon XR, the price of cct mother share is at 1.450. The nil paid rights price should be trading at 0.087 (1.45 - 1.363). If the price of the nil paid rights is way below 0.087, then the logical question to ask if this: is the mother share overvalued or the nil paid rights undervalued? It presents an arbitrage opportunity here. But this is advanced technique to play with rights, and it's highly advisable for newbies not to do it unless you know what you're getting into."

*These rights would actually appear on your CDP account.

---

3. Entitled Rights

You can find this by calculating from how many shares you have.

If you don't want to calculate manually, or want to confirm, wait for the Offer information statement (OIS) to be sent to you. In it, there'll be a circular on the whys of the rights exercise, and the how to the different scenario where a shareholder can subscribe to the rights. Most important, there will be a form where they will tell you explicitly how much rights you are entitled to. You can either fill the form, send a cheque and post it to them for rights subscription, or just ignore the form and go to the atm to subscribe for the rights.

Take note of the "Last date and time for acceptance" in the document. You MUST subscribe or they will expire worthless by this date.

You will get fractional allotments of rights, but rounded down. For example, if the right issue is 50 for every 1000 shares, you will still be allocated 25 rights if you have 500 shares.

---

4. Excess Rights

You can also subscribe to excess rights above and beyond your entitled rights.

For example, if you are entitled to 830 rights, you will definitely be able to get 830 new shares, because well, that's your entitlement. But for the excess rights, preference will be given to round off odd lots and the rest is luck.

So, if you apply for 70 excess, you will likely get it (to round off to the 100/share lot size).

How much to apply the maximize?

Suggestion is to just put 1.0 your holdings before XR. It's unlikely you will get excess rights beyond the number of shares you hold originally, especially for a good company rights issue.

Let's say you have 5000 shares and are entitled to 830 shares. You can just apply 5000 - 830 = 4170 excess rights. In total you are applying for 5000 rights (830 entitled and 4170 excess) and you would have to pay for it. The rest will be refunded to your account.

Link to step by step guide on using ocbc atm to subscribe for rights: here

---

5. Check Allocated Rights

Date is listed as expected date of crediting rights units, usually 1 day before commencement of trading for rights share. You can check the CDP account around night time to ensure that the rights shares are credited. If that's slow, try checking the refund in the bank account where you applied for the rights. From the amount of money refunded to you, you can back calculate to see how much excess rights you got. The slowest confirmation is after a few days, you will get a snail mail of the rights shares you get through your physical mail box.

---

6. Pro Forma Figures

The Pro Forma Figures is a set of important figures that are usually presented in the circulars about the rights issue. The pro forma figures are estimated values of important financial figures such as yield, gearing, NAV, revenue, net profit, etc, assuming the rights issue has been carried out at an earlier date, usually 1 year or 6 months ago.

The past financial figures will be adjusted accordingly to factor in the effect of the rights issue. It will factor in the reduction in interest payment for debts if the funds raised has been used to pay up loans. If the rights issue comes together with proposed acquisitions of new properties, then the increase in distributable income from these new properties will be factored in. Most importantly, the increase in total outstanding shares will be factored in when calculating the figures such as yield and NAV.

The pro forma figures is an important set of figures to look at if you want to estimate the diluting effect of the rights issue. The yield may decrease in the short term due to the increase in the share base, but the pro forma figures will give an idea of yield in the middle to long term after factoring in payment of debts and income from new acquisitions. However, do take note that these are estimated figures, and the actual figures may turn out better or worse.

Now that you know what are assets and why you want to buy assets, it's time to learn how to use assets to grow your money.

For starters, you need to know what is "risk free interest", the 3 main factors that differentiate assets and what are the common assets.

What is Risk Free?

First, we need to understand the concept of "risk free asset".

There is technically nothing in this world that is risk free. Countries can go bankrupt, currency can become worthless, a nuclear bomb could strike your city, aliens could invade Earth and everything could go to zero.

Hence, by risk free, we mean 99.9999% risk free. In case the unimaginable happen, it would be a doomsday scenario and you would have more to worry about than your assets becoming worthless.

The most common risk free asset in Singapore context would consist of things such as Singapore government issued bonds, CPF, etc. Think about it, if these things ever become worthless, that would mean the entire SG currency would be worthless.

Three Main Factors That Differentiate Assets

They are Returns (how much rewards you get), Risk (how much and what probability you stand to lose) and Liquidity (how easy it is to access/sell your asset without penalty).

It all seems very vague, but you will get an idea once I list some common assets.

Asset

Returns

Risk

Liquidity

Cash

None

Risk-Free

Very-High

Bank Savings

Very-Low

Risk-Free

High

CPF-OA

Low

Risk-Free

Low

CPF-SA

Med

Risk-Free

Very-Low

Singapore Saving Bonds

Very-Low

Risk-Free

High

Blue Chips Bonds

Low

Low

High

Blue Chips Shares

Med

Med

High

Penny Stock Shares

High

High

High

Investment Linked Policies

Low

Low

Low

As you can see, there are always trade-offs between the 3 factors. There is no assets that gives you high returns, risk-free (capital guaranteed) and let you withdraw anytime.

Think about it this way:

Suppose your bank saving account guarantee you super high returns similar to shares. Would anyone in their right mind invest in shares then?

Suppose CPF-SA grants you the ability to withdraw anytime. Would anyone in their right mind put their savings in banks? The logical thing would be to top up everything into CPF.

The "market' always adjusts itself.

Suppose you can choose to loan money to POSB Bank, or to a hardcore gambler. Both offer you 5% interest. Would you loan your money to the gambler? I guess not.

But what if the gambler promises you 20% returns? 50%? 100%? At what point would it be enticing enough for you to make the switch?

As you can see, the market will "correct" itself until the risk-returns (and liquidity) factors are balanced. This is how all free-markets (including stock market) works.

What Are Good Assets Then?

How good an assets is would greatly depend on your risk tolerance, how important is liquidity a factor for you, etc... Generally, a good asset should score highly in 2 of the categories.

For instance:

Blue chips gives you good returns with moderate risks and are highly liquid (sell anytime).

CPF gives you reasonable returns and are risk-free, but are non-liquid (many conditions).

A typical bad asset are investment linked policies.

While risk of it going kaput is low, it gives low returns (many just average 2 to 3% returns, much worse than stocks) and are highly non-liquid (you must keep paying premiums, once you stop you lose a lot, and you can't withdraw the money as you like).

Revenue dipped 1%, mainly due to AEI at Northpoint. Phase 2 is expected to complete in September, so I expect the next result to be similar. Shopper traffic is up ~3% if we exclude Northpoint.

All is well except Bedok Point, but I guess it can't be help at this time.

All eyes are now on the grand opening of Northpoint City. Rejoice Frasers shareholders!

Netlink Business Trust

Really small position due to IPO allocation.

Nothing much to say except this stock is not meant for flipping. This is a 5.7% yield dividend machine.

I expect very small fluctuations and investors to treat this more like a bond.

If in the unexpected case that it gets sell down harshly (to 70c), I will consider unleashing a full bullet. Otherwise, it'll probably just occupy a small position on my portfolio for a long time.

Sembcorp Industries

I thought the results was okay, considering the several one-offs deductions. Marine continue to be down in doldrums.

For Utilities, it is mainly supported by Singapore (50% of net profit) now. India's might continue to make losses for 2 to 3 years as they secure the power purchase agreement.

Interim dividend goes down to 3c, from 4c last year to build up their cash reserves.

Strategic revamp of the company will complete in 4Q.

M1

M1 posted another bad quarter (-20% profit) and is my most concerned counter at the moment. DPU has fallen to 11c, below my previous worst case estimate of 12c. I am strictly monitoring its performance.

Revenue is stable, fibre customers is climbing up slowly ($8K), data exceeding basic bundle is raising, and yet their profits keep falling. They are really squeezing their margins to retain their customers as can be seen from the falling ARPU.

My interpretation is that major shareholders refuse to sell at ~$2.1 due to low ball offers. Hence, the majority shareholders must felt that M1 is worth more than that.

I really have no confident in their CEO. Temasek selling is not a good sign as well. They are diversifying into data analytics, smart nation and IOT initiatives, but these all take time to become profitable.

Yield at $1.9 is 5.8%, based on trailing results.

Capital Commercial Trust

CCT has always been worry free for me. DPU inch up 4.6% despite office sector headwinds. I don't even pay attention to this due to confidence in its management and assets.

Main catalyst now is the redevelopment of Golden Shoe Complex.

The problem is I believe the fair value is $1.6, and now the price has gone up as high as $1.75. First world problem.

Accordia Golf Trust

This quarter gave me a confidence boost, being one of the better earnings for a while, with utilization and player numbers going 2 to 3% above 3 year average. Profit went up 10%. NAV dropped from 0.89 due to weaker Yen.

I really like their asset enhancement initiative slides which was pretty cool. GPS navigation systems, junior and ladies programmes, special events, collaboration with partners like car rentals. It gave a more 'story' perspective to their business instead of all numbers.

Far East Hospitality Trust

Property income dipped slightly to 1%, while DPU slide by 4%.

It will continue to be challenging in 2017 until hotel supply taper off and hopefully recovery in 2018.

Singtel

Singtel proves its resiliency compared to the other 2 Telco, and profit would have been up 3% if not been for intense competition at Airtel. While ARPU is lower (a macro trend), it is much higher at $65.

Its $2 billion profit from Netlink will be recorded in Q2.

Very safe 4.6+% yield and my largest position.

Frasers Centrepoint Ltd

Another good set of results.

Frankly, I'm treating this like a property ETF so I am not reading much into their individual segments.

70% of the assets and 50% of net profits are from recurring sources (i.e REITs), which provides a good "baseline" of dividends.

Dividends has been maintained at 8.6c for the past 3 years and I expect it to continue.

Capitaland Mall Trust

Capitaland Mall once again erases all rumors of "death of retail malls" in Singapore you see all over the news. Glad I did believe myself and brought in a substantial position. Its all about asset quality and location.

Despite the absence of Funan, they still manage to maintain their profits, shopper traffic and most importantly DPU.

Quite confident that their 11c, 5.5% yield is very safe until the grand opening of Funan.

I am not a professional investment guru; I'm a income machine builder.

Straits Times Index

DPU is back to 48c (2015 level). At current prices, yield is ~3%.

I've been trying dozen of ways to combat insomnia. Unfortunately, they only work from time to time, and in the worst case I still have to resort to sleeping pills.

---

1. Contract tightly, then relax your muscles starting from toes to head and back to toes.

2. Place tongue behind 2 front teeth. Breath in counts of 4, hold for 7 and breath out for 8. Do not assume regular breathing in between.

3. Use White Noise App (Slumber, Calm, Headspace)

4. Wearing socks

5. Glass of milk / Chamomile Tea / Banana

6. Lavender Oil Essence

7. Squeeze left first, release and repeat for right first, counting each as they were sheep.

8. Close your eyes and try your best to stay awake

9. Immerse your face in very cold water for 30 seconds

10. Practice left nostril breathing. Block off your right nostril with your right thumb and take long slow deep breaths through your left nostril only. This is said to have a soothing and relaxing effect on body mind in Yoga.

13. Take a warm bath or shower. Research show this can decrease body temperature and trigger sleepy feeling because your heart rate, digestion and other metabolic processes slow down.

Performance Highlights

Market continue its upward trajectory for the year and our portfolio went up by 5.2% for the quarter, compared to 3.8% of the STI, thanks to a couple of purchases we made. Our assessment is that Singapore Market is quite fairly valued now.

We paid out dividends of over $1000, slightly lesser than the same period less year due to the absence of ST Engineering & China Merchant Pacific. It is incredible that we have grown our passive income from less than $1K per year in 2014 to $1k every quarter in just 3 years.

Operating Highlights

Income for the quarter was about 10% higher than last year due to higher revenue and couple of mini items such as credit card cashback.

Earnings is expected to improve significantly in the 2nd half due to presence of bonus items.

Expenses were much lower (~40%) compared to same period last year, and just 5% higher compared to 2015. The only major expenses were as follow, which was really minimal:

- Father's A&E cost in April

- Niece's birthday, good quality replacement chair in May

- Friend's wedding in June

We do not forsee any major expense coming up except for our traditional gift to parents.

Acquisitions & Divestments

We went on the biggest acquisition spree ever (as guided) - firing 3 bullets which all were profitable as of now.

Singtel: We doubled down on this "bluest of blue chips" Telco when it went on sale due to fear from their Australia operations and 4th Telco entry. This is one investment where we have no fear piling on and it has now become our biggest holding (20%). A solid 4.8% dividend yield with Netlink IPO as a major catalyst.

Far East Hospitality Trust: We fired a medium-sized bullet for this and it went up despite the less than stellar results. This is a speculative bet we added mainly to gain exposure to the hospitality sector (which we do not have) which is pose for recovery. We can expect 7% yield or at least 6.5% in the very bad case.

Capitaland Mall Trust: The boat returns again for the trust and we were able to top up our partial fulfillment last quarter to turn this into a full solid position. We have confidence in their grade A malls, all conveniently located beside MRTs. While the fear of online shopping (Amazon, Alibaba) taking over is real, we think Plaza Singapura, Junction 8, Bugis Junction, Westgate, etc... will always have a place in our society. Retail will be transform to become more F&B and service oriented, and friends will still meetup for KTVs, movies, dinner at shopping malls. The ultimate catalyst for this is the transformation of Funan shopping Mall in 2019. For now, we expect a stable 5.8% yield.

For the first time in 3 years, our cash holdings actually went down for a quarter and our equities portfolio have crossed a major milestone.

Financial Strength

We are extremely comfortable with our level of warchest now, and will try to channel as much as possible all future income to investments. We expect to recover 2 bullets from our parent company in the next quarter, and a minor bonus in July, which will help refill our ammunition.

In May, we applied for SCB unlimited card with 2 year fee waiver until May 2019. Expected benefits: Spending $300 on OCBC365 would have gotten $1.0 cashback compared to SCB $4.50 now. We also got $100 vouchers on top of the $138 cashback!

We also just learnt that you can actually top up EZLink card using Credit Card. That's about $1.50 (enough for a free trip) every month, with even greater convenience. While people may laugh at this being negligible. remember that these are practically "free money" with almost no effort.

Outlook

The company will slowdown its expansion in the next quarter with at most 1 or 2 purchase. Currently, Netlink IPO, Comfort Delgro and SGX are on our watchlist.

August is another strong dividend month and Q3 will definitely be a great harvesting quarter.

I don't even know how I got into this "mess"... LOL.

I believe it started with me watching some "k-pop group dancing other group songs" on Weekly Idol...

And then coming across Pewdiepie's reaction to them, and the Blood Sweat & Tears video. Then clicking on some of the "recommended related videos".

Mistake man.

I clicked on Dope and that's the one that really got me hooked.

So much that I could not stop listening to the song and watching the MV

The choreography (that footwork) is absolutely captivating, the song (its bizarre and strangely addictive saxophone chorus), the ending, the MV, the lyrics (turn on the subtitles) everything is just so... dope.

"I reject rejection!"

Then it went to the dance practice videos, reaction videos and eventually to their other songs:

Fire, Not Today, Bapsae, Boys In Luv, War of Harmone, Danger...

It's freaking amazing how all their songs have such incredible choreography. I was never a fan of dancing, but they made it look like the coolest thing on the planet.

Perfectly sync, some godly moves (Fire climax is my favorite so far), executed extremely cleanly.

Then it went to joke/costume version of their dance, live performances to Bangtan bombs series.

I must have spent like 40 hours in the past week alone watching all these.

And I can't stop watching. I guess I'm part of the Army now.

LOL.

As far as I remember, this is the 3rd time I'm so obsessed with something from Korea.

I have no idea the cause - it's definitely not about feeling particularly stress.

In the past, it could be lying on bed until 3am. Or maybe waking up at 3am and being unable to sleep.

And somehow recently, it's getting worse. Absolute worst.

These days, I can simply toss and turn the entire night, straight until day break.

Doesn't matter weekday or weekends. It just strikes randomly.

I've tried sleep meditation videos and apps, the 4-7-8 breathing, the drinking milk/wearing socks, the blue screen filter, even as far as purchasing melatonin (natural sleeping chemical produced by our bodies), but yet the effects are minimal.

When it strikes, it strikes really hard and randomly. It's like I can never fell asleep once I past the golden hour (usually between 12 to 1am). Worst, this one last up to 2 or even 3 days.

This is the foundation and fundamental concept towards financial freedom.

Putting aside lottery and inheritance, there are only 2 ways you can make money:

1. Exchanging Time/Energy for Money, or Human Capital

2. Making Money From Money, or Financial Capital

Unfortunately, human capital is limited. We cannot work forever, and we only have 24 hours a day. Unless you are a super-high earner who can amass a fortune during your productive age on your job, you can never achieve financial freedom by the first method alone. This is because once you stop working, so does the cash inflow.

Most "commoners" are forever stuck with the first method. We were never taught other ways. If you do so, you will work until the day you die.

Take a moment to consider what would you rather have?

1. 20 Years of food in the warehouse

2. A farmland of livestock and crops that can produce enough food to feed you every year

1. $1 million dollars in the bank

2. Assets that can generate $50K per year, every year, forever.

The Chinese have a saying - "Even if you have a mountain of gold, it'll eventually dry up when you stop working." (做吃山空)

Hence, the way to financial freedom is not to accumulate a mountain of gold, but to collect things that can generate gold for you perpetually.

The ordinary man work for 40 years, save up loads of money and then hope it'll last him through his retirement until the day he leave Earth. The financial literate person accumulates assets until his assets generate enough cashflow to cover his expenses.

What's the difference?

The second method has some clear advantages: You are never afraid that you would “live too long”. There is no risk of you having to return to work when you are 80 years old cause your retirement fund run out. There is no risk of spending too much when you first cashout your retirement lump sum.

In other words: Grow apple trees, not collect apples. Buy cows, not milk. Buy chickens, not eggs.

So, what are assets? Assets are essentially anything that produces money/value. An asset generate cash inflow for you.

A simpler definition: If this thing gives you money, it’s an asset. If this thing takes money from you, it’s either an expense or liability.

A good dividend stock? It’s an asset.

A coupon-paying bond? It’s an asset

A milk-producing cow? It’s an asset.

Food that you need to eat? Expense.

Movie and entertainment? Expense.

Student loan? Liability.

Some often misinterpreted ones:

Your insurance/healthcare plan? It’s a liability.

Monthly car installment? It’s a liability.

A house you’re paying mortgage for? It’s a liability.

A house you rented out and collecting money every month? It’s an asset.

Certain things (like house) can be both an asset and liability at the same time. It's a complicated topic with many views but that's beyond the scope of this article. In essence, anything that does not give you money is an expense or liability (food, gadgets, clothings, etc...)

Remember this: The rich buy assets, not liabilities.

Everything is summarize by this guy.

The path to financial freedom is to have your money work for you.

The easiest to do this, for a typical Singaporean, is to use the first method (your human capital) to accumulate your first pot of gold. Save a lot, then invest it into assets.

Let your assets generate income, and use the income to buy more assets. (i.e 钱生钱)

In this diagram below, Poor Dad refer to the financially illiterate and majority of the population. Rich Dad is the path towards financial freedom.

Summary:

1) Work -> Income -> Buy Assets -> Repeat

2) Assets -> Generate Income -> Buy Assets -> Repeat

In your early years, most of your money will come from the first method. It can only be so for people who aren't born with a silver spoon, for commoners like us.

Thus, you need to make hay while the sun still shine. When you are young, your passive income will be pathetic compared to your active income. As you grow older, your human capital will eventually plateau and go into decline. You have less energy, are at greater risk of being fired, of becoming obsolete, of losing out to fresh graduates. That is the time when your financial capital should take over your human capital to generate money for you.

Eventually it will snowball to the point where income from the 2nd method covers your entire lifestyle expense.

And that, my friends, is financial independence.

A Side Note On Debt

Many young generation today live a "YOLO" lifestyle, thinking they should enjoy all they can, spending all their salary or worse, getting into debt.

Debt and liabilities are the greatest obstacle to financial independence. Debt is borrowing from your future self. Interests on debt are "reverse passive income" that will compound against you. Never get into debt.

Finally I leave you with this video from OnePercentBetter. This article covers Chapter 2.

NPI dipped 3% while DPU is maintained, largely due to Northpoint AEI. Northpoint will be complete in the later part of this year, and in my opinion its integration with Northpoint City will bring FCT to new heights.

Average rental revision at 4.1% which is impressive when you compare it to other REITs which are either incurring negative revision or flattish revision.

A slight concern to me is the 3.5% dip in shoppers traffic. We have to observe to see if this forms a trend.

Super Group

Divestment completed at $1.30 per share.

Sembcorp Industries

Profit goes up slightly thanks to land sales from Urban Development, but this is one off. Marine continue to suffer and Utilities was unexpectedly bad, particular the overseas segment.

Big news is new CEO plans to take 6 months for a strategic revamp of its operations.

M1

Profit continue to suffer (6th consecutive quarter) another 14%, with the usual culprits such as falling international call. 1Q EPS at 3.9c, down from 4.5c. M1 is sacrificing average revenue per user (ARPU) in exchange for maintaining/slightly increasing subscribers.

Losing faith with its management as they won't commit on dividend/profit guideline, sticking with "80% Payout".

Worst case, I am expecting 15c EPS and 12c DPU. At $2, it will be 6% yield.

Stock price is heavily influenced by the ongoing "shareholder review".

Capital Commercial Trust

Once again defy all expectations with 10% higher DPU despite the office rental headwinds.

Main catalyst now is the redevelopment of Golden Shoe Complex.

The price has run up a fair bit now, and I think it's now fairly valued at around $1.6.

Accordia Golf Trust

Unexpectedly bad results, with current DPU dropping over 14% to 4.71 yen for the whole year. Annual dividend (SGD) dropped 9% from 6.63c to 6.04c

This is attributed to higher snowfall in Feb.

Remains at a steep discount to book value of 0.91 and supported mainly by its yield.

ST Engineering

NA.

Crazy run up in prices!

Singtel

Showed resilliant results (net profit up 2%) when its peers are down in doldrums (both M1 and Starhub down 30 %).

Nothing much to say except I'm confident. Looking forward to Netlink IPO later this year.

Frasers Centrepoint Ltd

Really surprising results with net profits up 90% due to profit recognition from Suzhou, China and Singapore. FCL currently has about 46%, 33%, 9% and 7% assets in Singapore, Australia, China and Europe respective - and they are looking to increase investments in overseas assets for long term growth. It's a good diversification from SG for me.

70% of the assets and 50% of net profits are from recurring sources (i.e REITs), which provides a good "baseline" of dividends. Despite the relatively high level of debt, I am quite confident in its management.

Dividends has been maintained at 8.6c for the past 3 years (5.8% yield at $1.495, very high for a property developer).

Capitaland Mall Trust

Not much comments as position is extremely small.

Rental revision is almost flat.

Expect DPU to be stable around 11c until the return of Funan Mall in 2019.

In the first post of this series, I'm going to debunk why you should never grow your money with insurance companies, banks, managed funds, etc...

It's actually VERY SIMPLE.

Just ask yourself: Why are they wasting their time to help you manage your money? You think really got people so free? Why do you think there's always random strangers at the MRT stations offering to help you "earn more money"?

It doesn't take a genius to figure out - because they get a cut in the process. Commissions, management fees, you named it. If they don't earn anything, you think people got so much free time to waste on a stranger?

Always remember: Their purpose is to earn from you.

This immediately puts their interest and your interest in conflict.

Supposed there are 2 equal investment products, would they recommend you the one that cost less or more fee? If they take more percentage in fee, that means less returns for you. So are they working in your interest, or their interest?

It's nothing personal - it's just business.

It's just how the world of capitalism works.

Have you ever wonder why no insurance agents/financial consultant would ever recommend you to buy Singapore Saving Bonds (risk free 2%), or to buy term insurance (they get almost no commission), or putting your money in CPF?

Imagine how dumb that is.

It's like the meat-seller telling you "Don't eat meat already. You are overweight."

It's like housing agent telling you "Prices are high now you should wait."

It's like the shop uncle telling you "This item if cheaper if you get it from next door."

See the point?

I'm not saying what they recommend doesn't make sense. I'm saying 99.99% of the time (unless you have a saint for a financial consultant), what they recommend isn't optimal. Agents got to eat, you know?

It is inevitable that they will skew their recommendations towards higher commissioned products; Products that have much better alternatives. The same products that you can purchase elsewhere.

Suppose you want to buy Bread + Peanut Butter. You can:

1. Head to your local mart and buy them individually for $2 and $3.

2. Have your agent packed it in a hamper as 1 item, and sell it to you for $10.

This is investment-linked policies for you.

This is bank structured deposits for you.

This is managed funds for you.

They packaged everyday, simple financial products and sell you at a steep premium.

What these agents know are how to sell to you, not how to make good investments.

Those agents (sometimes fresh graduates) often know nothing more about investments than you.

So two points:

1. Their financial interests are in conflict with yours

2. They are not much better than you in investments in the first place

Don't believe? You will soon as we get further in this series.

It is like paying an ignorant person a commission to help you "grow" your money. You lose in 2 ways - You make lesser than you would have, and they get to take a cut of your capital with it. You are basically paying for underperformance, and these fees you pay add up massively over time.

So why are there still so many people who let people managed their money?

Mostly because they don't want to take responsibility for it. They are scare of losing when they make their own investments. They prefer someone else losing it for them, and thus having someone to blame for it.

1. No one care more about your finances except yourself.

2. You lose in multiple ways when you get someone to manage your money.

3. Financial ignorance will cost you much more over your lifetime than a few years of salary will.

"If you don’t understand the incentives of your advisor, you’re liable to discover that you’ve done wonders for his financial future while potentially wrecking your own.

This post is to bookmark down this page which is a huge gem.

It capture the essence of that blog and financial freedom. Aside from the more US-specific investment strategy, all the ideas written there are fantastic and applicable to Singapore.

The first 7 chapters are must read, especially on the market always going up and how fund managers rip us off.

"The market always, and I mean always, goes up. Not each year. Not each month. Not each week and certainly not each day. But relentlessly up." "The fact is only 20% of fund managers will beat the Index over time. 80% will fail. 100% of them will charge you high fees to try. There is no predicting which will be in that rarefied 20%.

Every fund prospectus carries this phrase: “Past results are not a guarantee of future performance.” It is the most ignored sentence in the whole document. It is also the most accurate."

And how we have become so accustomed to debt - the greatest obstacle to wealth building.

"If you intend to achieve financial freedom you are going to have to think differently. It starts by recognizing that debt should not be considered normal. It should be recognized as the vicious, pernicious destroyer of wealth-building potential it truly is. It has no place in your financial life."

Performance Highlights

The market went on a crazy bull run since the start of the year with STI exploding 300 points. Rising tides lift all boats and our portfolio leapfrogged 9.5% into positive territory after 2 years.

Looking back, we can only regret not pumping more capital into the market during the downturn, even though we are intrigued with the crazy run-up in US.

On a positive note, we paid out dividends of over $1000 (base on pay-date), highest ever for Q1 since inception.

Operating Highlights

As forecasted, income for the quarter were almost 40% lower than the same period last year. This was mainly due to:

- Absence of bonus in January and March.

- No Chinese New Year winnings (compared to Feb last year)

Earnings is expected to catch up in the following 3 quarters.

Expenses were about 16% higher compared to last year, but inline with 2 year average. This was mainly due to:

- Gambling losses during the CNY period (charged in January).

- Wedding events in February.

- Mayday Concert and board game purchase in March.

Acquisitions & Divestments

The market run-up means less opportunities, although we managed to nibble a tiny bit of CapitalMall Trust due to partial fulfillment. Lesson learnt: Do not be afraid to just buy at market value if we strongly believe in the purchase. In this case, we missed a substantial run up due to wanting to save $50.

Super Group was finally privatized and we let go of our holdings at a overall loss of 25%. A lesson for blindly buying at high prices and not having the conviction to average down after the shares plummet 50%. Thankfully, this is the smallest holding in our portfolio and the damage is minimal.

Bank Accounts

The unexpected bad news was yet another downgrade of OCBC360 account. Fortunately, we have maxed out our Maxigain counter (our plan 1 year ago finally bearing fruit) at 1.2% bonus interest. With rising US interest rates, SIBOR rate is also expected to trend up.

Considering these changes, our cash account rankings are as follow:

1. Citibank Maxigain: 0.55+% for the first month, ~1.75+% subsequently. Withdrawal conditions.

2. OCBC 360: 1.55%, 1.85% on certain months.

3. CIMB Fastsaver: 1% unconditional.

We are saddened by the change and have explored other options, but have not find any with a definitive advantage over OCBC360. This is because we are unable to the meet the $500 spending in most months which most other banks require.

For now, our immediate action is to reduce reliance on CIMB Fastsaver and direct more into our stock holdings to meet this year dividends goal. Any long term reserves will go straight into Maxigain, and OCBC360 will store our bullets.

We applied for the SCB Unlimited Cashback card with 1.5% rebate, which we believe present the best value for us at the moment. We will be closing the Bank of China account.

Financial Strength

DBS Vickers is currently having a major promotion with reduced commissions (0.12% with min $10, down from 0.18%) until June.

In other news, Budget 2017 announced tax rebate of 20% up to $500 this year, which would result in slightly lower tax expenses.

Our financial strength is at an all time high with more than 5 years of emergency funds and 10 years of warchest.

Outlook

Our immediate priority is to deploy cash as soon as reasonable opportunities come along before the strong dividend months of May and August arrive. Hopefully we can see some market corrections soon.

Barring unexpected circumstances, we expect higher dividends for the next 3 quarters.

This week, someone I know was administered into the hospital and I went to visit him.

There, I see many frail and old people.

Tubes and needles being inserted into them... It's a really saddening sight.

I think it's something people of my age don't really get to see often.

It's something we don't think about because we still have our youth and health.

...

I imagined the day when I would be lying down on one of these bed, looking back at what I have achieved.

When we were young, we were processed through the system to study. When we reached our 20s, we put off plans to pursue our interests to get into higher paying jobs. In our 30s or 40s, we delay plans to travel the world in order to build our families, to pay off our housing loans.

And then we continue to put off plans to pay for our kids university, to buy a bigger house, a bigger car, etc...

Before you knew it, we would be in our 60s.

By then, we would have lost most of our health and energy.

Do we really want a life where we only live to pursue more and more zeroes in our bank account? Or is this just some plan to enrich other people? Other people who created this "system" who made us think this is a normal life?

For me, I know when I will have enough.

Enough that I can tell myself: I won't be a burden to society or anyone. I can feed myself and live in contentment. And I will know it's time to quit the race. "How in the hell could a man enjoy being awakened at 6:30am by an alarm clock, leap out of bed, dress, force-feed, shit, piss, brush teeth and hair, and fight traffic to get to a place where essentially you made lots of money for somebody else and were asked to be grateful for the opportunity to do so?" - Charles Bukowski

If I recall correctly, this would be my first full year of attending the Board Games Meetup.

To date, I've played around 100 games of all kinds: Cooperative, deduction, classic-euro, negotiation, diplomacy, economic, dexterity, resource management, etc...

And for each game, you can learn all kind of "soft-skills", such as:

1. Expand your vocabulary and ability to link unrelated stuffs in Codenames.

2. Train your ability to keep a straight face and "sow discord" in Secret Hitler.

3. Test your imagination and judgement skills in Dixit.

4. Your negotiation and charisma to bring people to your side in I'm the Boss.

5. Your deduction, story-telling, teamwork and puzzle solving skills in Time Stories.

The list goes on.

I think "outsiders" are still stuck in the old days where they think Board Games = Monopoly, Scrabble and Uno.

Nowadays, there are much more variety of games that engages you in all aspects.

Recently, I've had the chance to play this game call "Panic on Wallstreet", a negotiation economic game based on luck and probability.

Playing this game, I can really feel the different styles that different kind of players adapt.

While most managers and investors play "by the rules" and negotiate in the pit, there are a couple who "strike up their own private deals". Instead of touting in the mass market, they build up their own network by personally approaching investors.

This builds up "rapport" and "regular customers" which they can take advantage of, where they have less fear of failing to sell their stocks. On the other hand, time pressure can often force managers to let go of their properties at ridiculously low-price.

We have master mathematicians who try to bid for deals where they will "never lose" (at most break-even), and master negotiators who try to squeeze every inch of juice out from the other party.

I just feel it's amazing that I can see such diverse attitudes and styles towards a simple game that simulate the real world.

Come across this fascinating article about the supposed life of every Singaporean, and the author rebuttal against it.

My thoughts?

When you want 5 star hotel wedding, take 30 year loan for million dollar condo, buy big car, go annual vacation to Europe/US, change latest iphone every year, how to save for retirement?

Chinese have this saying: No so big head, don't wear so big hat. If you are a peasant (and earn a peasant income), don't try to live an elite life.

No doubt there are people truly living in poverty in Singapore (don't earn enough to even put 3 meals on table, much less save), but also got lot of cases is people die die want to buy something they can't afford (throw all their savings/take on big debts for car and house) and then claim they nothing left for retirement.

I don't deny the cost of living in Singapore is extremely high, but I think that gives us even more reason to be prudent with our earnings.

"Rich people stay rich by living like they're broke. Poor people stay poor by living like they're rich."

I can only shrug my shoulders when I see people who are lazy to even write a form to credit their salary to a higher interest account (a one time effort and gets you free money).

- You and your dependents (family), are generally healthy and does not have long term and huge medical bills.

- Your family does not depend on you for survival, and you do not have to spend a huge portion of your income on them.

- You income is not too low (Subjective, but I would say below 2.5K)

In my opinion, most graduates from middle income family would have no problem meeting these criteria.

1. Study hard, get a good degree, earn a median income and try to have as high of a saving rate as possible, especially in your 20s (the first 5 year is crucial).

2. If applicable, clear all your debts ASAP, do not rack up credit card or any other debt, and do not waste money on useless shit. Do not take debt to go on vacation, buy liabilities and other non-income producing crap.

3. Save up emergency fund of 6 months, and put them in a high interest account. Then start saving for your warchest. Try to hit 1 year annual saving before 30s. This immediately gives you passive income of $1.2K per year (or ~$100 per month).

4. Start investing properly and correctly. Even if you are extremely conservative, you should get around 5% return over the long term.

5. Earn money -> invest -> collect dividends -> re-invest your dividends. Keep repeating this for the next 10 years.

7. If you follow this diligently, by the time you're in your 40s, your investment (passive income) can easily cover more than half of your expenses (saving rate ~50%). If your saving rate is truly insane (>70%), you might even reach financial independence here. If you haven't, continue doing step 5 for the next 10 years and you would achieve the same. It's all up to your saving rate at this point.

8. As a guideline, aim to have minimum 1 year annual income of savings by 30s. 5 by 40s, 10 by 50s.

If you are willing to even put in a little effort to learn right investing, optimize your savings, and don't over indulge in luxuries, I am very sure most can achieve FIRE within 20 years. Many local bloggers have achieved it much much earlier on median income, in their 30s even. So 20 years is a really conservative estimate already.

Problem is, are people willing to put in the effort?