Key Highlights & Notes From CEO

"Financial Freedom Is Not About Money, It’s About Living Your Best Life"

Every day, we build our portfolio bit by bit, brick by brick, for the ultimate goal of escaping the rat race in the not so distant future.

This has been arduous year with many challenges in the market, but despite the setback we still took significant steps towards FIRE. We completed our 2nd year in the new job, continued steady capital injections and broke multiple financial milestones.

1. Total net asset value grew 16%

2. Highest ever annual saving rate of 80.8% (80.5% in 2017, 78.2% in 2016)

3. Safety passive income now cover 65% of our recurring expenses (41% in 2017, 28% in 2016)

4. Portfolio market value grew 38% (inclusive of capital injection and gains)

5. Portfolio XIRR for 2017 at -10.17% (20.8% gain in 2017, 15.6% gain in 2016)

6. By XD-Date, distributed over $7800 worth of dividends ($4900 in 2017, $3200 in 2016)

Our Balance Sheet (2018)

Going forward, we would measure our balance sheet by how long we can sustain ourselves if all cash inflow were to stop today. All figures are based on trailing 12 months average.

Survival Burn Rate = Recurring expenses needed for essential survival

LEAN FI Rate = Expenses needed to maintain our current lifestyle

FI Rate = Lifestyle with built-in buffer that we want to achieve in Financial Independence

Our next milestone goal is to attain the holy grail of "25 years annual expenses" - the classic and minimal definition of Financial Independence. Numbers fell in 2018 due to significant increase in our expenses, which is likely to continue rising every year. Despite this, we are confident of reaching this milestone latest by end Year 2021.

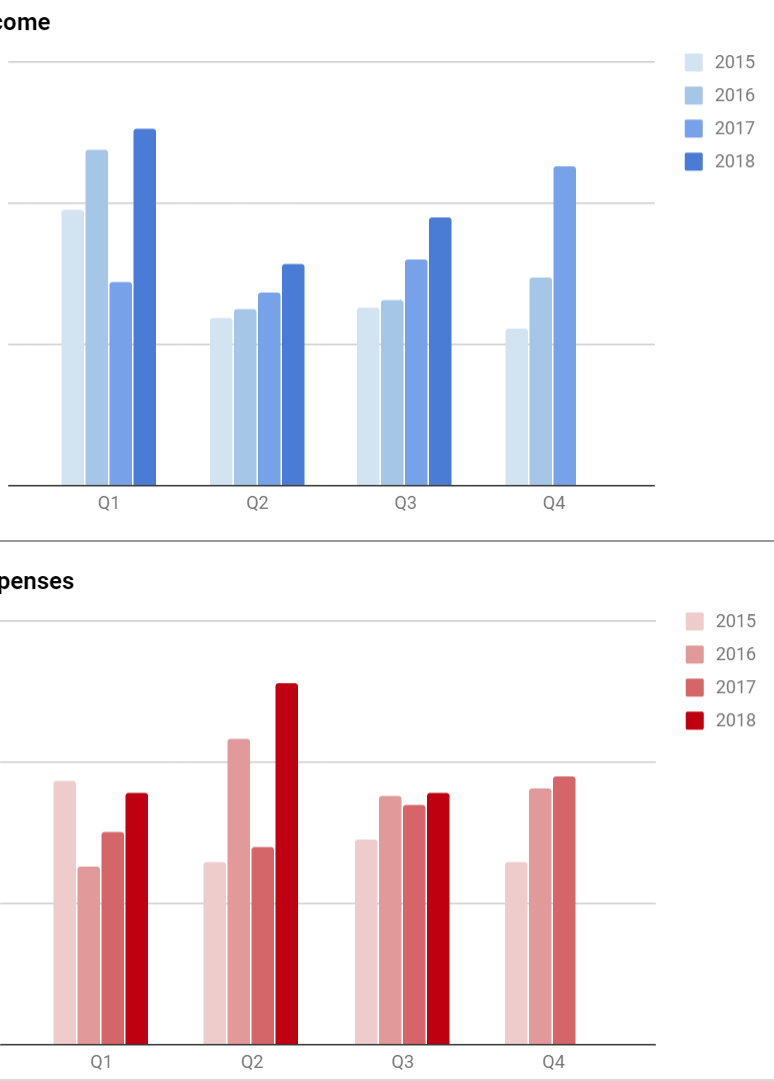

Income Statement

Total income was 27% higher than last year - our highest growth rate since inception. Operating income was 22% higher, driven by higher base salary and bonus.

Passive income increased 40% and now makes up >13% of our total income - thanks to huge dividends growth, switch to DBS Multiplier and increasing SIBOR rate for Maxigain.

Expenses were around 25% higher and also our highest year mostly due to 1-time expenses, especially from April vacation and insurance policies. We expect 1-time expense to trend even higher in 2019 as we take over all policies. Recurring expenses were in-line at right around the average of past 3 years.

*All figures exclude CPF and investment capital gains/losses.

-------------------------------------------------------------------------------------------------------------------------Saving Rate For 2018

2018 marked our highest income, expense and saving rate year ever. Saving rate inched up another 0.3% from last year. Assuming no change to main revenue, we expect our saving rate to remain above 80%.

-------------------------------------------------------------------------------------------------------------------------

Recurring Expenses Breakdown

Categorical expenditures remained pretty much the same as every year. Top expenditures were the essentials - food, travel (transport) and utilities (internet and phone).

Random discovery time!

1. Lottery spending in 2018 was around $350 ($50 higher than 2017), yet I won back much lesser at $15 ($80 in 2017). There goes my annual $300 donation to Singapore Pools.

2. I ate fast food 64 times (70 in 2017, 81 in 2016), counting only lunch, dinner, supper, with an average of $7.5 per meal. It is getting lesser, and I am hoping to keep it below 60 in 2019.

3. I brought 22 (11 in 2017, 31 in 2016) cups of Bubble Tea (i.e Koi, Gong Cha) this year. This was probably due to more brands entering the market and the "need" to try them all... Still I think this number is consider low among my friends.

4. I brought 4 cups of Cafe drinks (Starbucks, Coffee Bean) but this figure is high distorted. There are many "lower-end starbucks" and "pop-up stores" that I brought drinks from which were not tagged.

5. Visited restaurants 32 times (20 in 2017), but a handful of trips were just to utilize vouchers. Discounting these, each restaurant trip only averaged $14 - proving that I mostly stucked with "low-class restaurant" like Ajisan and Swensens. Even the most expensives meals cost just $20+.

6. Only 10 KTV sessions this year! Anyone want go sing? :(

Passive income grew more than 60%! Equities valuation were definitely more attractive compared to 2017 and granted us good opportunities to take huge leaps forward.

-------------------------------------------------------------------------------------------------------------------------

Our worst year since inception with a XIRR of -10.2%, underpforming the STI by almost 4%. Despite this, we still grew the size of by 38% thanks to the staggering amount of capital injection.

| Year | Portfolio | ES3 |

|---|---|---|

| 2014 | -2.94% | 7.00% |

| 2015 | -8.17% | -10.95% |

| 2016 | 11.97% | 3.08% |

| 2017 | 22.00% | 21.11% |

| 2018 | -10.40% | -6.63% |

Majority of our losses came from Kimly and Singtel, offset by the privitization offer of M1.

Our major holdings currently are Singtel, Kimly and the STI. Excluding the STI, we have a healthy and diversified portfolio of 11 holdings (up from 10 last year and 8 in 2016).

-------------------------------------------------------------------------------------------------------------------------

Review of 2018 Goals

We far exceeded our 2018 goal of $500/mth of dividends and hit over $600/mth.

Expenses were 25% higher (projected 10%) on the back of insurance policies and major loss in 2018Q1.

Outlook For 2019

We will continue our core strategy of building up a divesified income portfolio backed by index foundation. We are more than 10 year into the bull-run and the music got to stop one day.

Once again, our ammunition have replenished entirely after December, and would fatten even more in March. Hopefully we have opportunities to deploy them before the dividends season come in Q2.

This year goal would be to exceed $10,000 worth of dividends - an ambitious and lofty goal, so hopefully we get some Great Singapore Sale. Current SGXCafe projection stands at $8000.

There is a good chance of a income source switch which would definitely have impact on revenue. For now, we would let nature take its course.

2019 is the year we completely take over insurance policies from our parent company, so we expect expenses to rise quite signicantly. Holidays are on the card as well, but nothing too lavish.

Long Term Goals

Depending on when the great correction/meltdown occur, we intend to soon diversify into the global markets. By the end of this year, we should have solidified our local portfolio. Letting it grow any larger would placed great exposure and expections on Singapore Economy.

Although I am personally confident in Singapore, I still could not risk placing all our money in 1 basket. What if we experience a lost decade like Japan?

Some long term directions, likely to start in 2020:

- Open Interactive Brokers Account (Start with DCA and within 2 years grow it to more than $100K USD when we can enjoy $10 platform fee waiver)

- Indexing World ETF via IWDA + EIMI (Currently near 1-year low and we would definitely go in should it drop to lower $40s). Both ETFs automatically reinvest dividends (i.e accumulating units).

- Indexing for China via Heng Seng Index (HK 2800). China growth in the next 20 years should be immense.

- Local portfolio reached substantial size to start lending shares for extra income

Our long term roadmap:

Year 2019: Continuing to build up recurring expense buffer.

Year 2020: Start diversifying into global markets.

Year 2021: Reach "25 Years Expense" Networth.

Year 2022: Eligibility to buy HDB.

Year 2023: Passive income completely cover all-expenses. Save 100% of salary annually.

Year 2025: Financial Independence.

Our major holdings currently are Singtel, Kimly and the STI. Excluding the STI, we have a healthy and diversified portfolio of 11 holdings (up from 10 last year and 8 in 2016).

Review of 2018 Goals

We far exceeded our 2018 goal of $500/mth of dividends and hit over $600/mth.

Expenses were 25% higher (projected 10%) on the back of insurance policies and major loss in 2018Q1.

Outlook For 2019

We will continue our core strategy of building up a divesified income portfolio backed by index foundation. We are more than 10 year into the bull-run and the music got to stop one day.

Once again, our ammunition have replenished entirely after December, and would fatten even more in March. Hopefully we have opportunities to deploy them before the dividends season come in Q2.

This year goal would be to exceed $10,000 worth of dividends - an ambitious and lofty goal, so hopefully we get some Great Singapore Sale. Current SGXCafe projection stands at $8000.

There is a good chance of a income source switch which would definitely have impact on revenue. For now, we would let nature take its course.

2019 is the year we completely take over insurance policies from our parent company, so we expect expenses to rise quite signicantly. Holidays are on the card as well, but nothing too lavish.

Long Term Goals

Depending on when the great correction/meltdown occur, we intend to soon diversify into the global markets. By the end of this year, we should have solidified our local portfolio. Letting it grow any larger would placed great exposure and expections on Singapore Economy.

Although I am personally confident in Singapore, I still could not risk placing all our money in 1 basket. What if we experience a lost decade like Japan?

Some long term directions, likely to start in 2020:

- Open Interactive Brokers Account (Start with DCA and within 2 years grow it to more than $100K USD when we can enjoy $10 platform fee waiver)

- Indexing World ETF via IWDA + EIMI (Currently near 1-year low and we would definitely go in should it drop to lower $40s). Both ETFs automatically reinvest dividends (i.e accumulating units).

- Indexing for China via Heng Seng Index (HK 2800). China growth in the next 20 years should be immense.

- Local portfolio reached substantial size to start lending shares for extra income

Our long term roadmap:

Year 2019: Continuing to build up recurring expense buffer.

Year 2020: Start diversifying into global markets.

Year 2021: Reach "25 Years Expense" Networth.

Year 2022: Eligibility to buy HDB.

Year 2023: Passive income completely cover all-expenses. Save 100% of salary annually.

Year 2025: Financial Independence.