Frasers Centrepoint Trust | NPI dipped 3% while DPU is maintained, largely due to Northpoint AEI. Northpoint will be complete in the later part of this year, and in my opinion its integration with Northpoint City will bring FCT to new heights. Average rental revision at 4.1% which is impressive when you compare it to other REITs which are either incurring negative revision or flattish revision. A slight concern to me is the 3.5% dip in shoppers traffic. We have to observe to see if this forms a trend. |

Super Group | Divestment completed at $1.30 per share. |

Sembcorp Industries | Profit goes up slightly thanks to land sales from Urban Development, but this is one off. Marine continue to suffer and Utilities was unexpectedly bad, particular the overseas segment. Big news is new CEO plans to take 6 months for a strategic revamp of its operations. |

M1 | Profit continue to suffer (6th consecutive quarter) another 14%, with the usual culprits such as falling international call. 1Q EPS at 3.9c, down from 4.5c. M1 is sacrificing average revenue per user (ARPU) in exchange for maintaining/slightly increasing subscribers. Losing faith with its management as they won't commit on dividend/profit guideline, sticking with "80% Payout". FY 2015 DPU: 15.3c, EPS: 19c FY 2016 DPU: 12.9c, EPS: 16.1c Worst case, I am expecting 15c EPS and 12c DPU. At $2, it will be 6% yield. Stock price is heavily influenced by the ongoing "shareholder review". |

Capital Commercial Trust | Once again defy all expectations with 10% higher DPU despite the office rental headwinds. Main catalyst now is the redevelopment of Golden Shoe Complex. The price has run up a fair bit now, and I think it's now fairly valued at around $1.6. |

Accordia Golf Trust | Unexpectedly bad results, with current DPU dropping over 14% to 4.71 yen for the whole year. Annual dividend (SGD) dropped 9% from 6.63c to 6.04c This is attributed to higher snowfall in Feb. Remains at a steep discount to book value of 0.91 and supported mainly by its yield. |

ST Engineering | NA. Crazy run up in prices! |

Singtel | Showed resilliant results (net profit up 2%) when its peers are down in doldrums (both M1 and Starhub down 30 %). Nothing much to say except I'm confident. Looking forward to Netlink IPO later this year. |

Frasers Centrepoint Ltd | Really surprising results with net profits up 90% due to profit recognition from Suzhou, China and Singapore. FCL currently has about 46%, 33%, 9% and 7% assets in Singapore, Australia, China and Europe respective - and they are looking to increase investments in overseas assets for long term growth. It's a good diversification from SG for me. 70% of the assets and 50% of net profits are from recurring sources (i.e REITs), which provides a good "baseline" of dividends. Despite the relatively high level of debt, I am quite confident in its management. Dividends has been maintained at 8.6c for the past 3 years (5.8% yield at $1.495, very high for a property developer). |

Capitaland Mall Trust | Not much comments as position is extremely small. Rental revision is almost flat. Expect DPU to be stable around 11c until the return of Funan Mall in 2019. |

Straits Times Index | NA |

Thursday, May 25, 2017

Quarterly Results Review - 2017Q1

Wednesday, May 10, 2017

ZZ Financial Education Series 1 - No One Care About Your Money Except Yourself

If you ask the butcher if you should have meat or veg today, what would he say?

If you ask the salesgirl if the shoes look good on you, what would she say?

If you ask the insurance agent if you are sufficiently covered, what would he say?

If you ask the property agent is it better to invest in stocks or property, what would he say?

If you ask the broker if it is a good time to buy stocks now, what would he say?

If you ask the barber if you need a haircut, what would he say?

...

DON'T ASK STUPID QUESTIONS LAH!

A property agent agent job is to sell house, not to take care of your finances.

An insurance agent job is to sell insurance & earn commission, not to take care of your finances.

---------------------------------------------------------------------------------

In the first post of this series, I'm going to debunk why you should never grow your money with insurance companies, banks, managed funds, etc...

It's actually VERY SIMPLE.

Just ask yourself: Why are they wasting their time to help you manage your money? You think really got people so free? Why do you think there's always random strangers at the MRT stations offering to help you "earn more money"?

It doesn't take a genius to figure out - because they get a cut in the process. Commissions, management fees, you named it. If they don't earn anything, you think people got so much free time to waste on a stranger?

Always remember: Their purpose is to earn from you.

This immediately puts their interest and your interest in conflict.

Supposed there are 2 equal investment products, would they recommend you the one that cost less or more fee? If they take more percentage in fee, that means less returns for you. So are they working in your interest, or their interest?

It's nothing personal - it's just business.

It's just how the world of capitalism works.

Have you ever wonder why no insurance agents/financial consultant would ever recommend you to buy Singapore Saving Bonds (risk free 2%), or to buy term insurance (they get almost no commission), or putting your money in CPF?

Imagine how dumb that is.

It's like the meat-seller telling you "Don't eat meat already. You are overweight."

It's like housing agent telling you "Prices are high now you should wait."

It's like the shop uncle telling you "This item if cheaper if you get it from next door."

See the point?

I'm not saying what they recommend doesn't make sense. I'm saying 99.99% of the time (unless you have a saint for a financial consultant), what they recommend isn't optimal. Agents got to eat, you know?

It is inevitable that they will skew their recommendations towards higher commissioned products; Products that have much better alternatives. The same products that you can purchase elsewhere.

Suppose you want to buy Bread + Peanut Butter. You can:

1. Head to your local mart and buy them individually for $2 and $3.

2. Have your agent packed it in a hamper as 1 item, and sell it to you for $10.

This is investment-linked policies for you.

This is bank structured deposits for you.

This is managed funds for you.

They packaged everyday, simple financial products and sell you at a steep premium.

You still want to buy from them?

Up to you lor.

---------------------------------------------------------------------------------

To add on, these people aren't necessary more savvy than you in the first place.

Every now and then you see news of agents themselves getting scammed.

What these agents know are how to sell to you, not how to make good investments.

Those agents (sometimes fresh graduates) often know nothing more about investments than you.

So two points:

1. Their financial interests are in conflict with yours

2. They are not much better than you in investments in the first place

Don't believe? You will soon as we get further in this series.

It is like paying an ignorant person a commission to help you "grow" your money. You lose in 2 ways - You make lesser than you would have, and they get to take a cut of your capital with it. You are basically paying for underperformance, and these fees you pay add up massively over time.

So why are there still so many people who let people managed their money?

Mostly because they don't want to take responsibility for it. They are scare of losing when they make their own investments. They prefer someone else losing it for them, and thus having someone to blame for it.

---------------------------------------------------------------------------------

In Summary:

1. No one care more about your finances except yourself.

If you ask the salesgirl if the shoes look good on you, what would she say?

If you ask the insurance agent if you are sufficiently covered, what would he say?

If you ask the property agent is it better to invest in stocks or property, what would he say?

If you ask the broker if it is a good time to buy stocks now, what would he say?

If you ask the barber if you need a haircut, what would he say?

...

DON'T ASK STUPID QUESTIONS LAH!

A property agent agent job is to sell house, not to take care of your finances.

An insurance agent job is to sell insurance & earn commission, not to take care of your finances.

---------------------------------------------------------------------------------

In the first post of this series, I'm going to debunk why you should never grow your money with insurance companies, banks, managed funds, etc...

It's actually VERY SIMPLE.

Just ask yourself: Why are they wasting their time to help you manage your money? You think really got people so free? Why do you think there's always random strangers at the MRT stations offering to help you "earn more money"?

It doesn't take a genius to figure out - because they get a cut in the process. Commissions, management fees, you named it. If they don't earn anything, you think people got so much free time to waste on a stranger?

Always remember: Their purpose is to earn from you.

This immediately puts their interest and your interest in conflict.

Supposed there are 2 equal investment products, would they recommend you the one that cost less or more fee? If they take more percentage in fee, that means less returns for you. So are they working in your interest, or their interest?

It's nothing personal - it's just business.

It's just how the world of capitalism works.

Have you ever wonder why no insurance agents/financial consultant would ever recommend you to buy Singapore Saving Bonds (risk free 2%), or to buy term insurance (they get almost no commission), or putting your money in CPF?

Imagine how dumb that is.

It's like the meat-seller telling you "Don't eat meat already. You are overweight."

It's like housing agent telling you "Prices are high now you should wait."

It's like the shop uncle telling you "This item if cheaper if you get it from next door."

See the point?

I'm not saying what they recommend doesn't make sense. I'm saying 99.99% of the time (unless you have a saint for a financial consultant), what they recommend isn't optimal. Agents got to eat, you know?

It is inevitable that they will skew their recommendations towards higher commissioned products; Products that have much better alternatives. The same products that you can purchase elsewhere.

Suppose you want to buy Bread + Peanut Butter. You can:

1. Head to your local mart and buy them individually for $2 and $3.

2. Have your agent packed it in a hamper as 1 item, and sell it to you for $10.

This is investment-linked policies for you.

This is bank structured deposits for you.

This is managed funds for you.

They packaged everyday, simple financial products and sell you at a steep premium.

You still want to buy from them?

Up to you lor.

---------------------------------------------------------------------------------

To add on, these people aren't necessary more savvy than you in the first place.

Every now and then you see news of agents themselves getting scammed.

What these agents know are how to sell to you, not how to make good investments.

Those agents (sometimes fresh graduates) often know nothing more about investments than you.

So two points:

1. Their financial interests are in conflict with yours

2. They are not much better than you in investments in the first place

Don't believe? You will soon as we get further in this series.

It is like paying an ignorant person a commission to help you "grow" your money. You lose in 2 ways - You make lesser than you would have, and they get to take a cut of your capital with it. You are basically paying for underperformance, and these fees you pay add up massively over time.

So why are there still so many people who let people managed their money?

Mostly because they don't want to take responsibility for it. They are scare of losing when they make their own investments. They prefer someone else losing it for them, and thus having someone to blame for it.

---------------------------------------------------------------------------------

In Summary:

1. No one care more about your finances except yourself.

2. You lose in multiple ways when you get someone to manage your money.

3. Financial ignorance will cost you much more over your lifetime than a few years of salary will.

"If you don’t understand the incentives of your advisor, you’re liable to discover

that you’ve done wonders for his financial future while potentially wrecking your own.

"If you don’t understand the incentives of your advisor, you’re liable to discover

that you’ve done wonders for his financial future while potentially wrecking your own.

- Tony Robbins"

You Can't Beat The Market

Do you want to add more wealth to your hedge fund managers, insurance agents, financial consultants?

Then watch this video.

"Remember, we have choices in life. While we still have time on our side, choose wisely."

Then watch this video.

"Remember, we have choices in life. While we still have time on our side, choose wisely."

Saturday, April 29, 2017

JJ Colin Stock Series

This post is to bookmark down this page which is a huge gem.

It capture the essence of that blog and financial freedom. Aside from the more US-specific investment strategy, all the ideas written there are fantastic and applicable to Singapore.

The first 7 chapters are must read, especially on the market always going up and how fund managers rip us off.

"The market always, and I mean always, goes up. Not each year. Not each month. Not each week and certainly not each day. But relentlessly up."

"The fact is only 20% of fund managers will beat the Index over time. 80% will fail. 100% of them will charge you high fees to try. There is no predicting which will be in that rarefied 20%. Every fund prospectus carries this phrase: “Past results are not a guarantee of future performance.” It is the most ignored sentence in the whole document. It is also the most accurate."

And how we have become so accustomed to debt - the greatest obstacle to wealth building.

"If you intend to achieve financial freedom you are going to have to think differently. It starts by recognizing that debt should not be considered normal. It should be recognized as the vicious, pernicious destroyer of wealth-building potential it truly is. It has no place in your financial life."

It capture the essence of that blog and financial freedom. Aside from the more US-specific investment strategy, all the ideas written there are fantastic and applicable to Singapore.

The first 7 chapters are must read, especially on the market always going up and how fund managers rip us off.

"The market always, and I mean always, goes up. Not each year. Not each month. Not each week and certainly not each day. But relentlessly up."

"The fact is only 20% of fund managers will beat the Index over time. 80% will fail. 100% of them will charge you high fees to try. There is no predicting which will be in that rarefied 20%. Every fund prospectus carries this phrase: “Past results are not a guarantee of future performance.” It is the most ignored sentence in the whole document. It is also the most accurate."

And how we have become so accustomed to debt - the greatest obstacle to wealth building.

"If you intend to achieve financial freedom you are going to have to think differently. It starts by recognizing that debt should not be considered normal. It should be recognized as the vicious, pernicious destroyer of wealth-building potential it truly is. It has no place in your financial life."

Sunday, April 02, 2017

Letter To Shareholders (6) - Performance Review 2017Q1

Performance Highlights

The market went on a crazy bull run since the start of the year with STI exploding 300 points. Rising tides lift all boats and our portfolio leapfrogged 9.5% into positive territory after 2 years.

Looking back, we can only regret not pumping more capital into the market during the downturn, even though we are intrigued with the crazy run-up in US.

On a positive note, we paid out dividends of over $1000 (base on pay-date), highest ever for Q1 since inception.

Operating Highlights

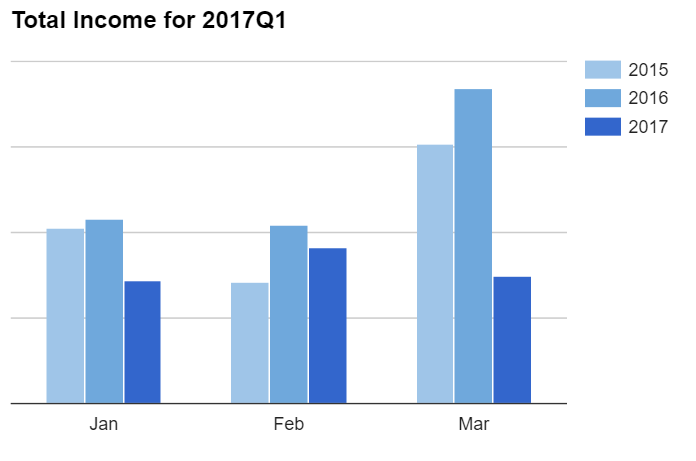

As forecasted, income for the quarter were almost 40% lower than the same period last year. This was mainly due to:

- Absence of bonus in January and March.

- No Chinese New Year winnings (compared to Feb last year)

Earnings is expected to catch up in the following 3 quarters.

Expenses were about 16% higher compared to last year, but inline with 2 year average. This was mainly due to:

Expenses were about 16% higher compared to last year, but inline with 2 year average. This was mainly due to:

- Gambling losses during the CNY period (charged in January).

- Wedding events in February.

- Mayday Concert and board game purchase in March.

Acquisitions & Divestments

The market run-up means less opportunities, although we managed to nibble a tiny bit of CapitalMall Trust due to partial fulfillment. Lesson learnt: Do not be afraid to just buy at market value if we strongly believe in the purchase. In this case, we missed a substantial run up due to wanting to save $50.

Super Group was finally privatized and we let go of our holdings at a overall loss of 25%. A lesson for blindly buying at high prices and not having the conviction to average down after the shares plummet 50%. Thankfully, this is the smallest holding in our portfolio and the damage is minimal.

Bank Accounts

The unexpected bad news was yet another downgrade of OCBC360 account. Fortunately, we have maxed out our Maxigain counter (our plan 1 year ago finally bearing fruit) at 1.2% bonus interest. With rising US interest rates, SIBOR rate is also expected to trend up.

Considering these changes, our cash account rankings are as follow:

1. Citibank Maxigain: 0.55+% for the first month, ~1.75+% subsequently. Withdrawal conditions.

2. OCBC 360: 1.55%, 1.85% on certain months.

3. CIMB Fastsaver: 1% unconditional.

We are saddened by the change and have explored other options, but have not find any with a definitive advantage over OCBC360. This is because we are unable to the meet the $500 spending in most months which most other banks require.

For now, our immediate action is to reduce reliance on CIMB Fastsaver and direct more into our stock holdings to meet this year dividends goal. Any long term reserves will go straight into Maxigain, and OCBC360 will store our bullets.

We applied for the SCB Unlimited Cashback card with 1.5% rebate, which we believe present the best value for us at the moment. We will be closing the Bank of China account.

Financial Strength

DBS Vickers is currently having a major promotion with reduced commissions (0.12% with min $10, down from 0.18%) until June.

In other news, Budget 2017 announced tax rebate of 20% up to $500 this year, which would result in slightly lower tax expenses.

Our financial strength is at an all time high with more than 5 years of emergency funds and 10 years of warchest.

Outlook

Our immediate priority is to deploy cash as soon as reasonable opportunities come along before the strong dividend months of May and August arrive. Hopefully we can see some market corrections soon.

Barring unexpected circumstances, we expect higher dividends for the next 3 quarters.

The market went on a crazy bull run since the start of the year with STI exploding 300 points. Rising tides lift all boats and our portfolio leapfrogged 9.5% into positive territory after 2 years.

Looking back, we can only regret not pumping more capital into the market during the downturn, even though we are intrigued with the crazy run-up in US.

On a positive note, we paid out dividends of over $1000 (base on pay-date), highest ever for Q1 since inception.

Operating Highlights

As forecasted, income for the quarter were almost 40% lower than the same period last year. This was mainly due to:

- Absence of bonus in January and March.

- No Chinese New Year winnings (compared to Feb last year)

Earnings is expected to catch up in the following 3 quarters.

- Gambling losses during the CNY period (charged in January).

- Wedding events in February.

- Mayday Concert and board game purchase in March.

The market run-up means less opportunities, although we managed to nibble a tiny bit of CapitalMall Trust due to partial fulfillment. Lesson learnt: Do not be afraid to just buy at market value if we strongly believe in the purchase. In this case, we missed a substantial run up due to wanting to save $50.

Super Group was finally privatized and we let go of our holdings at a overall loss of 25%. A lesson for blindly buying at high prices and not having the conviction to average down after the shares plummet 50%. Thankfully, this is the smallest holding in our portfolio and the damage is minimal.

Bank Accounts

The unexpected bad news was yet another downgrade of OCBC360 account. Fortunately, we have maxed out our Maxigain counter (our plan 1 year ago finally bearing fruit) at 1.2% bonus interest. With rising US interest rates, SIBOR rate is also expected to trend up.

Considering these changes, our cash account rankings are as follow:

1. Citibank Maxigain: 0.55+% for the first month, ~1.75+% subsequently. Withdrawal conditions.

2. OCBC 360: 1.55%, 1.85% on certain months.

3. CIMB Fastsaver: 1% unconditional.

We are saddened by the change and have explored other options, but have not find any with a definitive advantage over OCBC360. This is because we are unable to the meet the $500 spending in most months which most other banks require.

For now, our immediate action is to reduce reliance on CIMB Fastsaver and direct more into our stock holdings to meet this year dividends goal. Any long term reserves will go straight into Maxigain, and OCBC360 will store our bullets.

We applied for the SCB Unlimited Cashback card with 1.5% rebate, which we believe present the best value for us at the moment. We will be closing the Bank of China account.

Financial Strength

DBS Vickers is currently having a major promotion with reduced commissions (0.12% with min $10, down from 0.18%) until June.

In other news, Budget 2017 announced tax rebate of 20% up to $500 this year, which would result in slightly lower tax expenses.

Our financial strength is at an all time high with more than 5 years of emergency funds and 10 years of warchest.

Outlook

Our immediate priority is to deploy cash as soon as reasonable opportunities come along before the strong dividend months of May and August arrive. Hopefully we can see some market corrections soon.

Barring unexpected circumstances, we expect higher dividends for the next 3 quarters.

Subscribe to:

Posts (Atom)